Nice — below is a compact, slide-ready market reference for the High-Integrity Pressure Protection System (HIPPS) market arranged exactly to your headings and ending with a short company reference with values table you can drop into a slide or report. I pulled recent market reports, vendor pages and standards guidance so each load-bearing statement has a source you can cite.

This versatile research report is presenting crucial details on market relevant information, harping on ample minute details encompassing a multi-dimensional market that collectively maneuver growth in the global Inertial Measurement Unit market.

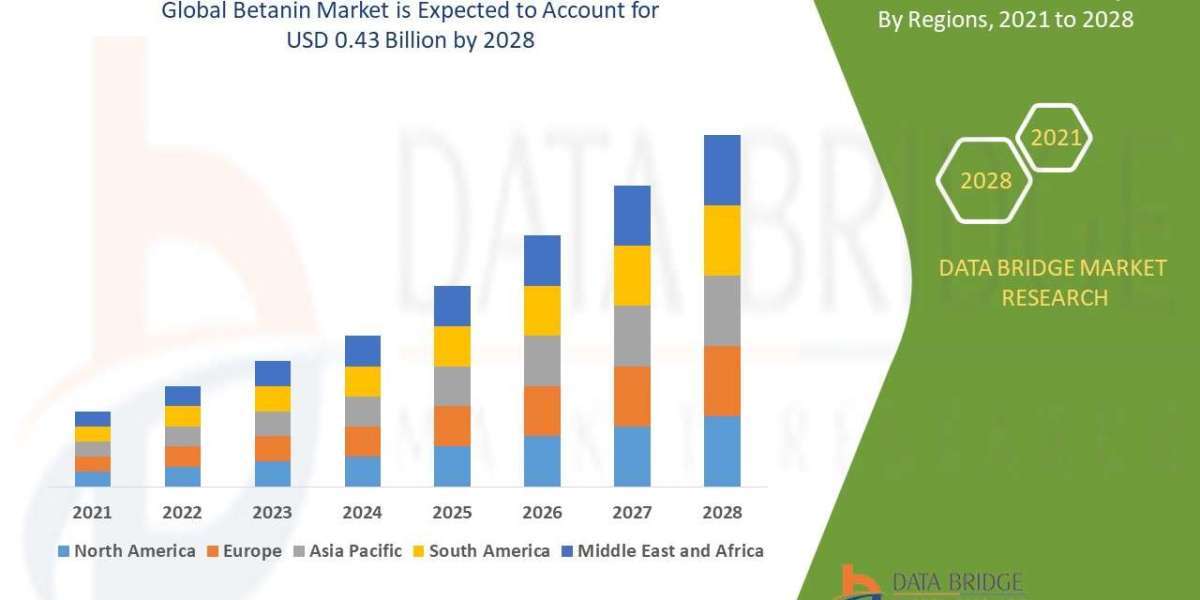

Read complete report at: https://www.thebrainyinsights.com/report/inertial-measurement-unit-market-14461

Market snapshot (high-level)

Reported market-size estimates vary with scope (SIS/HIPPS components vs. turnkey HIPPS solutions). Recent published values cluster in the USD ~0.5B → USD 1.1B (early-2020s) band with forecast CAGRs commonly in the ~5–8% range (varies by provider). Pick one forecasting house for a single number on a slide.

Five load-bearing facts (use on an executive slide)

HIPPS adoption is driven by process-industry safety regulation and the desire to avoid flare/venting — HIPPS can prevent hazardous releases by shutting upstream sources instead of relying on relief/flare systems.

Many HIPPS installations are designed and certified to SIL 3 per IEC 61508 / IEC 61511 — this guides architecture, voting, diagnostics and proof-test regimes.

Asia-Pacific and Middle East (LNG / upstream pockets) are top growth regions due to new build & retrofit projects; APAC often shows the fastest CAGR in market reports.

Market growth is supported by brownfield modernization (safety upgrades), LNG expansion, and tighter environmental/flare-reduction economics.

Vendor landscape mixes large automation/OEM groups (Emerson, Yokogawa, ABB, Schneider, Honeywell, Siemens, Rockwell) with specialist HIPPS/valve/skid suppliers and valve OEMs (mechanical HIPPS providers).

Recent Development

Renewed HIPPS adoption linked to LNG and petrochemical project pipelines and to operators seeking to reduce flaring/venting (environmental and commercial drivers). Several market reports (2024–2025) highlight stronger investment in HIPPS as part of SIS upgrades.

Emergence of pre-engineered skid HIPPS and mechanical HIPPS (fast-acting valve solutions) to shorten lead times and simplify verification for certain applications.

Drivers

Regulatory & safety drivers (IEC 61508/61511, process safety audits, permits), plus cost of lost product & environmental fines.

LNG, petrochemical and upstream projects (high-pressure flows require overpressure protection without flaring).

Brownfield modernization (retrofit HIPPS vs. upgrading relief systems) and digital instrumentation that improves diagnostics and proof-testing.

Restraints

Higher capital and lifecycle cost vs simple relief devices (engineering, SIL proof, testing, maintenance).

Complexity of SIL verification, third-party certification (TÜV/Exida) and long qualification times for safety-critical systems.

Not suitable for all overpressure scenarios — some applications still require conventional relief and flare systems or combined approaches.

Regional segmentation analysis

Asia-Pacific: fastest growth in many reports — driven by China, India, Southeast Asia LNG & refining projects.

Middle East & Africa: strong demand from upstream, LNG and large refinery complexes.

North America: retrofit and offshore/upstream safety projects; strong presence of systems integrators and certification activity.

Europe: mature market with strict process safety enforcement and refinery/chemical upgrades.

Emerging Trends

Mechanical HIPPS (valve/actuator assemblies built to high integrity) and hybrid mechanical-electronic HIPPS for selected applications.

Pre-skidded, modular HIPPS packages to accelerate installation and simplify validation.

Digitalization of proof testing and diagnostics (better diagnostic coverage, remote proof-test scheduling, predictive maintenance) and attention to cybersecurity on safety systems.

Top Use Cases

Protecting downstream low-pressure equipment (separators, compressors, pipelines) from upstream overpressure.

High-pressure gas export lines and LNG mainlines where venting is undesirable.

Compressor anti-surge protection, flare minimization strategies, and cases where relief capacity is impractical.

Major Challenges

Achieving required SIL 3 performance with acceptable spurious trip rates (balancing safety vs operability).

Ongoing proof-testing and maintenance logistics (valve reliability, solenoid/actuator diagnostics).

Integration between HIPPS and broader SIS / emergency response systems and ensuring cybersecurity for connected safety assets.

Attractive Opportunities

LNG export & import projects, brownfield safety upgrades and decarbonization-driven flare reduction programs.

Modular/standardized HIPPS packages sold to EPCs and contractors for faster deployment.

Value-added services: proof-test-as-a-service, remote diagnostics, spare-parts bundles and end-to-end safety lifecycle management.

Key factors of market expansion

Pace of new LNG, petrochemical and upstream projects; regulatory enforcement of process safety; economics of flare reduction; and uptake of digital proof-testing & diagnostics.

Major companies — reference list with short “value” statements

(1-line each: company → what they bring to HIPPS / safety protection)

Emerson (Fisher / DeltaV / Safety Systems) — full automation and HIPPS skid solutions; value: integrated SIS/HIPPS with strong engineering & global service network.

Yokogawa — process automation + safety systems & HIPPS offerings; value: SIS integration and project delivery for refineries & LNG.

HIMA (safety controllers) / Rockwell / Schneider / Siemens — safety PLCs, logic solvers and system integration for HIPPS architectures; value: certified SIL logic platforms.

ABB — instrumentation, skid packages and safety systems; value: instrumentation + actuator solutions for fast shutoff and HIPPS implementation.

Honeywell — SIS/HIPPS system integration and lifecycle services; value: long history in process-industry safety and comprehensive service offerings.

Specialist valve & mechanical HIPPS suppliers (IMI Truflo / IMI STI / Maverick Valves / other valve OEMs) — mechanical HIPPS elements and fast-acting valve assemblies; value: proven valve technology and mechanical HIPPS options.

System integrators & EPCs (Schlumberger / Baker Hughes / local EPCs) — deliver full skid and project integration for large projects; value: project execution and commissioning expertise.

Note: the HIPPS supply chain mixes global automation majors (Emerson, Yokogawa, ABB, Honeywell, Schneider, Siemens, Rockwell) with specialist safety-PLC vendors (HIMA), valve OEMs/mechanical HIPPS providers and regional EPCs. If you want, I can produce a concise CSV of the companies above with Region | Core Product | Typical Application.

If you’d like one of these built immediately (I’ll make it now into a downloadable file):

a 1-page PPT (market snapshot + 3 suggested visuals + company table),

a CSV table: Company | Region | Value/Offering, or

a 1-page competitor matrix (companies × strengths: logic solvers, valves, skid packages, services).

Which output do you want me to build right away?