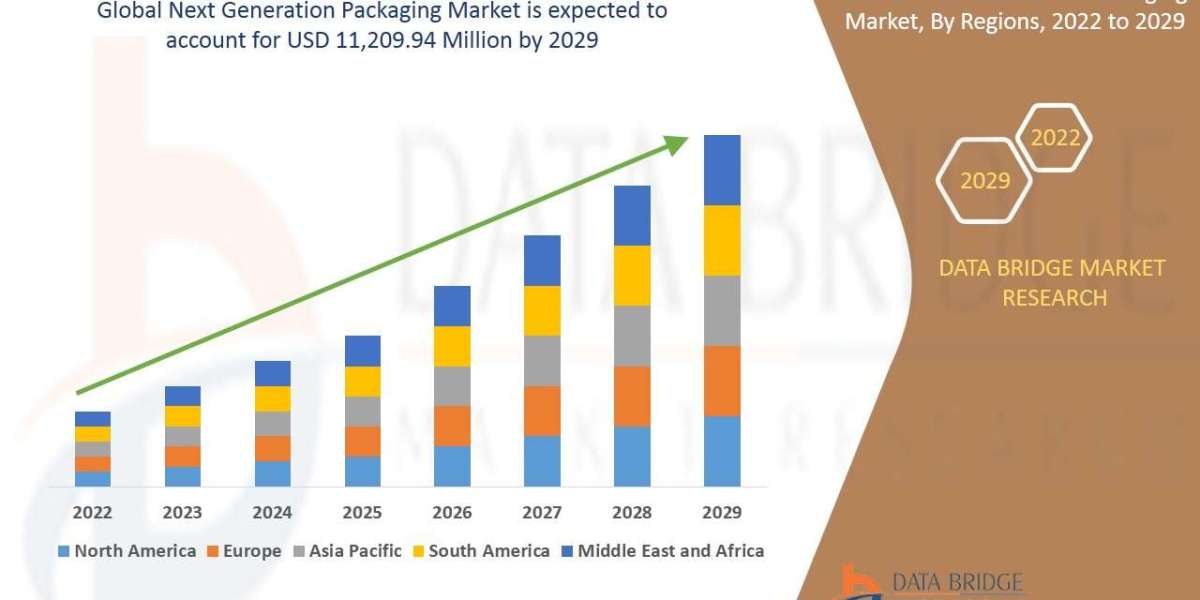

here’s a compact, source-backed market reference for the Paper Diagnostics market (paper-based diagnostics / lateral-flow / point-of-care paper diagnostics), with company references and the public “values” I could find (financial anchors). I prioritized recent company filings and industry reports so the load-bearing facts are cited.

This versatile research report is presenting crucial details on market relevant information, harping on ample minute details encompassing a multi-dimensional market that collectively maneuver growth in the global Paper Diagnostics market.

This holistic report presented by the report is also determined to cater to all the market specific information and a take on business analysis and key growth steering best industry practices that optimize million-dollar opportunities amidst staggering competition in Paper Diagnostics market.

Read complete report at: https://www.thebrainyinsights.com/report/paper-diagnostics-market-14082

Market snapshot (select figures)

Global market size (2024 / 2025 estimates): ~USD 17–18.5 billion (2024) with forecasts to ~USD 29–31B by early-to-mid 2030s (CAGRs ~6–7%). — Precedence Research estimate: USD 17.43B (2024); USD 18.51B (2025), CAGR ≈6.2%.

Lateral flow assays (LFAs) are the largest subsegment (typically ~40–50% share of “paper diagnostics” in most market reports).

Key companies (reference + available values / anchors)

Note: most large diagnostics firms report aggregate diagnostics revenue across many product types (not always broken out as “paper diagnostics” alone). I list the firms repeatedly named in LFA/paper diagnostics reports and attach public revenue anchors where available.

Roche (Diagnostics Division) — Diagnostics sales: CHF 14.324 billion in 2024 (Roche Annual Report 2024). Roche is a top global diagnostics player (molecular lab, POC & some rapid tests).

Abbott Laboratories — Company total sales: $42.0 billion (FY 2024). Abbott is a leading rapid test & LFA vendor (BinaxNOW, Alinity platform). Abbott reports COVID-testing related sales separately (e.g. ~$747M in COVID testing-related sales for full-year 2024), showing how much of “rapid test” revenue can be COVID-linked.

Thermo Fisher Scientific / Danaher / Beckman / Becton Dickinson / Bio-Rad / QuidelOrtho / bioMérieux / Hologic / QIAGEN — frequently listed among top LFA/POC players in market reports (company diagnostics revenues are large but not all attributable to paper diagnostics). See aggregated company lists in market reports.

Component & substrate suppliers (critical to paper diagnostics): Ahlstrom (specialty membranes / filtration materials), Sartorius / Merck KGaA / Cytiva / Sartorius — these companies supply nitrocellulose, backing pads, conjugates and are strategic for supply security. Ahlstrom reported record 2024 financial performance and notes growth in medical/specialty materials.

Large regional OEMs / contract manufacturers (China / India / regional players): Zhejiang Orient Gene, Hangzhou AllTest, Shenzhen Mindray, Axiva, DCN Diagnostics, Cobetter, etc. — important for volume and price-sensitive procurement.

Quick interpretation of “values”: Roche’s Diagnostics CHF 14.324B (2024) is the clearest, direct diagnostics-division value available publicly. Abbott’s $42B is company total and the company reported ~$747M COVID rapid test sales in 2024 — useful anchors for relative scale. Vendor revenue specifically for “paper diagnostics” is rarely broken out publicly — most vendor numbers are in diagnostics segments that include instruments, reagents and other tests.

Recent developments

Post-COVID normalization: test volumes for COVID have fallen from peak; firms rebalanced portfolios toward multiplex infectious-disease LFAs, cardiac/biomarker LFAs, and non-COVID applications.

Reader & connectivity push: greater investment in smartphone/reader attachments and cloud integration to improve clinical value and data reporting for LFAs.

Supply-chain focus on membranes & reagents: substrate suppliers (e.g., Ahlstrom) and specialty materials companies are strengthening supply reliability and capacity.

Drivers

Need for low-cost, decentralized testing in LMICs and community screening programs.

Ongoing infectious-disease surveillance and routine POC needs (respiratory, malaria, dengue, HIV, hepatitis).

Technology improvements (multiplex LFAs, better antibodies, digital readers, CRISPR/paper microfluidics R&D).

Restraints

Variable clinical performance among low-cost kits — regulatory/clinical skepticism limits uptake for certain applications.

Price competition from regional low-cost OEMs; procurement price pressure limits margins.

Regional segmentation (high level)

North America: largest revenue share / highest per-unit pricing and reader adoption.

Europe: mature, quality/regulation-driven buyers — strong for reader-enabled tests.

Asia-Pacific: fastest growth by CAGR (large population, many local OEMs; strong volume demand).

Latin America / MEA: smaller but rising demand aligned with infectious disease burden and donor programs.

Emerging trends

Multiplex paper LFAs (multiple analytes on one strip).

CRISPR / enzyme-amplified paper tests moving toward early commercialization (higher sensitivity POC molecular).

Connected readers / telemedicine integration for result capture and surveillance.

Top use cases

Rapid infectious disease screening (SARS-CoV-2, influenza, malaria, dengue, HIV).

Home/self-testing & pharmacy POC (pregnancy, fertility, strep, COVID).

Low-resource clinical diagnostics & field epidemiology (NGO/donor programs).

Major challenges

Sensitivity/specificity gaps vs lab molecular gold standards for many analytes.

Regulatory variability & need for local validation across many countries.

Margin pressure from commoditization and low-cost manufacturers.

Attractive opportunities

Digital + reader ecosystems (higher clinical acceptance; subscription/data services).

Higher-sensitivity paper molecular tests (CRISPR/enzymatic amplification) — if costs can be kept low, opens clinical markets currently dominated by lab PCR.

Secure, local supply of substrates (partner with Ahlstrom / Merck / Sartorius or invest in membrane capacity).

Key factors for market expansion (summary)

Sustained public health demand + surveillance budgets, tech advances (multiplexing, CRISPR, readers), and stable substrate supply chains will drive growth; main brakes remain regulatory/evidence hurdles and upward price pressure/competition.