This versatile research report is presenting crucial details on market relevant information, harping on ample minute details encompassing a multi-dimensional market that collectively maneuver growth in the global Medical Laser Systems market.

This holistic report presented by the report is also determined to cater to all the market specific information and a take on business analysis and key growth steering best industry practices that optimize million-dollar opportunities amidst staggering competition in Medical Laser Systems market.

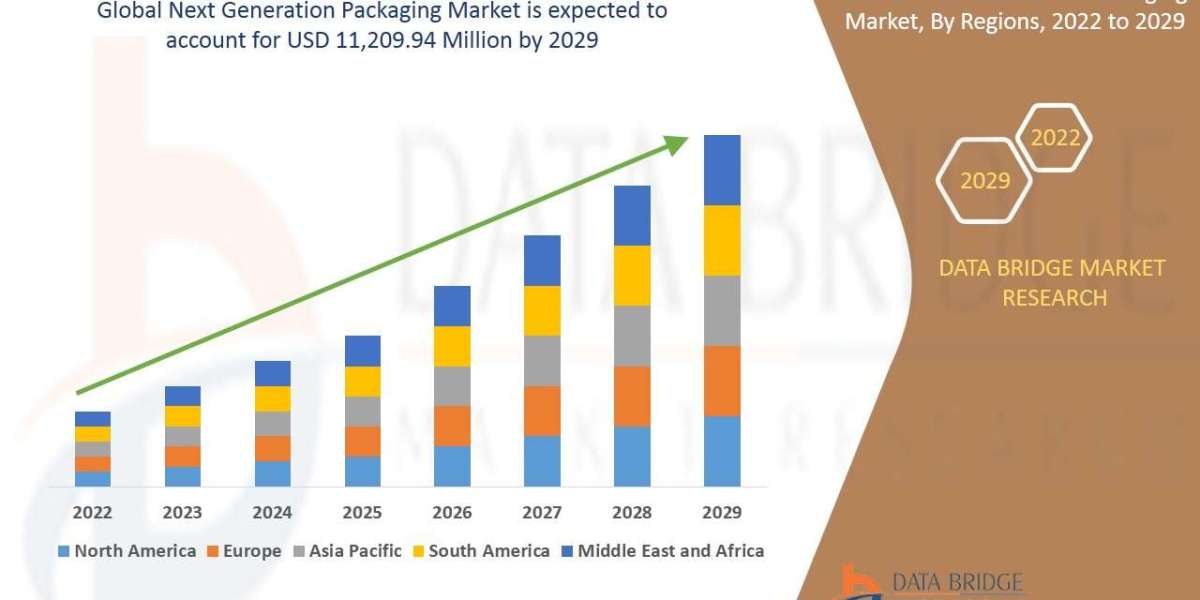

Read complete report at: https://www.thebrainyinsights.com/report/medical-laser-systems-market-12872

Company references (confirmed values)

Coherent (formerly II-VI / Coherent Corp.) — Laser revenue reported $1,469 million (FY 2023 lasers revenue) with breakdowns across industrial/instrumentation end markets in their annual filing.

El.En. S.p.A. — consolidated group financials published in the 2024 Annual Report (full report available; consolidated revenues and key P&L/EBITDA figures provided).

Cutera, Inc. — public company guidance and reported results; company expected 2024 revenue guidance $160–170M (Cutera Q4 / FY releases).

IRIDEX Corporation — reported FY 2024 revenue ≈ $48.7M (down from $51.9M in 2023) in its FY 2024 results.

BIOLASE, Inc. — public filings and press releases show small-cap dental/medical laser revenues (company reporting continued revenue commentary for 2023; full Form 10-K / annual filings available).

Fotona and Candela — widely cited major players in aesthetic and surgical lasers; Fotona publicly highlights record revenues in press notes and Candela disclosures/filings describe historical revenue and product lines (many aesthetic-laser market reports list them as top competitors).

Market sizing & recent developments (high level)

Market-size consensus (selection of recent reports): global medical laser systems market ≈ USD 4.8–5.1 billion (2023–2024) with forecasts ranging to ~USD 8–12B by 2028–2033 depending on scope and CAGR assumptions (reports from MarketsandMarkets, Databridge, MarketNtel/others). Typical forecasted CAGRs are mid-single to low-double digits.

Recent developments: demand rebound in elective aesthetic procedures post-COVID, sustained investment in ophthalmic/dermatology/urology lasers, and supplier capacity/technology investments (coatings, diode/solid-state innovations).

Drivers

Rising demand for minimally invasive & aesthetic procedures (dermatology, hair removal, body contouring, ophthalmology).

Technological advances — faster diode sources, solid-state lasers (Er:YAG, Nd:YAG), novel cooling/coating technologies improving uptime and outcomes.

Growing geriatric population & chronic-disease procedures that use lasers (e.g., ophthalmology, ENT).

Restraints

High capital cost of premium laser systems and consumable/maintenance costs for clinics.

Regulatory approvals & reimbursement variability across geographies slow adoption cycles in some clinical segments.

Fragmented end-user buying patterns (aesthetics clinics vs hospitals) create uneven demand and price sensitivity.

Regional segmentation analysis

North America — large market share (high elective procedure volumes, established reimbursement for certain procedures).

Europe — mature market with strong device vendors (El.En., others) and high adoption in dermatology/ophthalmology.

Asia-Pacific — fastest growth (China, India, South Korea) driven by rising aesthetic demand and expanding healthcare infrastructure.

Emerging trends

Hybrid & multi-wavelength platforms (single systems covering multiple indications).

Compact diode and portable systems enabling point-of-care and smaller clinic adoption.

Service/consumable recurring-revenue models (maintenance contracts, disposables).

AI-assisted treatment planning and integrated imaging are early but growing trends.

Top use cases

Aesthetic dermatology (hair removal, resurfacing, vascular/vein treatments).

Ophthalmology (retinal, glaucoma, refractive surgery — specialized lasers).

Dental & oral surgery (BIOLASE products focus here).

Urology / ENT / surgical ablation (Nd:YAG, CO₂ lasers).

Major challenges

Competition from lower-cost alternatives (non-laser modalities or cheaper imported systems).

Capital cycles: clinic purchasing delays during economic slowdowns.

Clinical training & credentialing — adoption depends on physician confidence & training programs.

Attractive opportunities

Aesthetic market expansion (non-invasive procedures growing rapidly).

Ophthalmic/retinal laser adoption tied to aging populations and diabetic-retinopathy screening programs.

Emerging markets (India, Latin America) — local distributors and lower-cost models to gain share.

Service-led offerings (RTU-like bundles, financing, training) to unlock mid-market clinics.

Key factors of market expansion

Procedure volume growth in aesthetics, ophthalmology and specialties.

Technology innovation that reduces downtime/increases throughput and applications per device.

Greater affordability & financing models for clinics (leasing, pay-per-use).

Regulatory approvals and evidence generation that broaden indications and reimbursement.

Want this as a ready table or slide?

I can immediately produce either:

an Excel table (company | last reported revenue | segment focus | notable product/technology | citation links), or

a one-page PDF/slide with market sizing chart + top 6 competitor snapshot.

Which output would you like? I’ll generate it right away and attach the file.