This versatile research report is presenting crucial details on market relevant information, harping on ample minute details encompassing a multi-dimensional market that collectively maneuver growth in the global Phototherapy Equipment market.

This holistic report presented by the report is also determined to cater to all the market specific information and a take on business analysis and key growth steering best industry practices that optimize million-dollar opportunities amidst staggering competition in Phototherapy Equipment market.

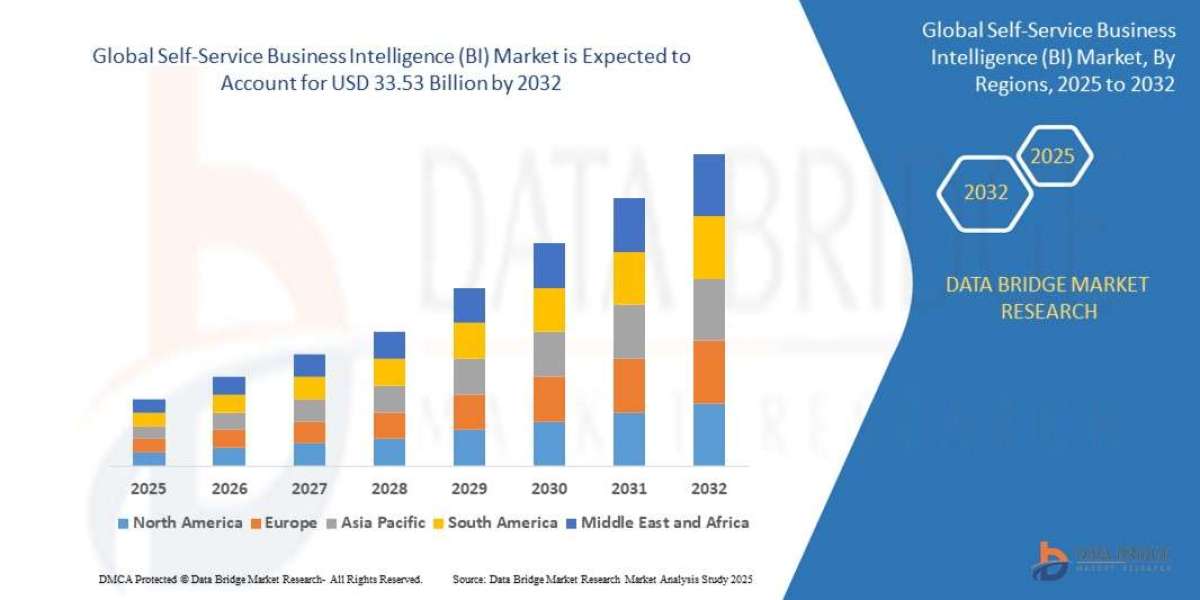

Read complete report at: https://www.thebrainyinsights.com/report/phototherapy-equipment-market-13671

Quick company references (who matters + product/value notes)

Natus Medical / NeoBlue — strong specialist in neonatal phototherapy (neoBLUE LED series for jaundice). Product-focused leader in neonatal phototherapy devices (LED overhead and portable systems). Example product page and product claims (LED lifetime, intensity).

GE Healthcare (Giraffe family) — major hospital-grade phototherapy systems (Giraffe Blue Spot, high-intensity spot and full-field phototherapy for neonatal care). Widely used in NICU settings.

Royal Philips (BlueControl and newborn care lineup) — wearable/LED dermatology phototherapy (BlueControl for plaque psoriasis) and broader neonatal/newborn device portfolio and consumables. Philips markets both dermatology (home/wearable) and newborn phototherapy products.

BTL Industries — maker of LED-based devices used in dermatology & aesthetics (LED/phototherapy products used in clinics). Corporate revenue snapshots available in regional filings (example: BTL India FY2024 revenue ~₹63.9 Cr).

Other notable vendors (appear repeatedly in market reports and vendor lists): Atom Medical (neonatal phototherapy), PARI / smaller specialist LED phototherapy manufacturers and some regional OEMs. Aggregators and market-report lists also cite additional device-specialist vendors.

Recent developments

Rapid shift to LED (from fluorescent/halogen) across neonatal and dermatology segments — LEDs offer longer life, targeted wavelengths, and lower maintenance.

Growth in portable and home-use phototherapy (wearable blue-light devices for dermatology; compact neonatal units for step-down or homecare). Philips BlueControl and other wearable/portable solutions highlight this trend.

Drivers

High incidence of neonatal jaundice and large patient populations (driving neonatal phototherapy demand).

Rising prevalence of skin disorders (psoriasis, vitiligo, eczema) and wider adoption of light-based dermatology treatments.

LED technology adoption (energy efficiency, maintenance savings) and product innovations (wearables, targeted wavelengths).

Restraints

Fragmented product definitions & inconsistent market scope (neonatal vs dermatology vs aesthetic phototherapy) — complicates procurement and sizing.

Price sensitivity in some emerging markets and slower replacement cycles for hospital capital equipment.

Regulatory and clinical-evidence requirements (safety/efficacy for home-use wearable devices) can slow rollout in certain regions.

Regional segmentation (high-level)

North America — large installed base (NICUs, dermatology clinics), strong hospital procurement and adoption of advanced LED systems.

Europe — mature market for clinical and dermatology phototherapy; strong adoption of wearable dermatology devices in some countries.

Asia-Pacific & Latin America — fastest growth potential driven by birth rates (neonatal needs), expanding healthcare access, and rising dermatology service demand; price sensitivity favors portable/affordable LED models.

Emerging trends

LED-first product strategies (longer life, lower operating cost).

Wearables & home phototherapy for dermatology (patient convenience + adherence data potential).

Hospital-to-home continuum — neonatal/step-down units and compact overhead LED units for small facilities and homecare.

Top use cases

Neonatal jaundice treatment (NICU overhead and phototherapy bassinets).

Dermatology (psoriasis, vitiligo, eczema) — clinic and home wearable phototherapy.

Aesthetic & allied clinic uses (adjunct LED therapy in dermatology / aesthetics clinics).

Major challenges

Report inconsistency: widely varying market estimates by vendor/report due to differing definitions — careful scope alignment is needed for commercial/strategic decisions.

Clinical validation for new home devices (wearables must demonstrate safety and outcomes vs clinic-based phototherapy).

Attractive opportunities

Affordable LED neonatal units for emerging markets (replace older ballast-based systems).

Connected wearable phototherapy + adherence services (subscription/SaaS models for dermatology).

Consumables & service contracts (NICU installations require support, consumables, and replacement lighting modules) — recurring revenue streams for vendors.

Key factors for market expansion (summary)

Clear, consistent market definitions (neonatal vs dermatology vs aesthetic) to guide sizing and product development.

LED technology adoption (cost, maintenance, wavelength control) and clinical evidence for home-use devices.

Reimbursement/healthcare access in emerging markets and stronger distribution partnerships for lower-cost devices.